The Market Price of Belief.

Between the retail price and the resale price, there is a gap. The gap is called belief.

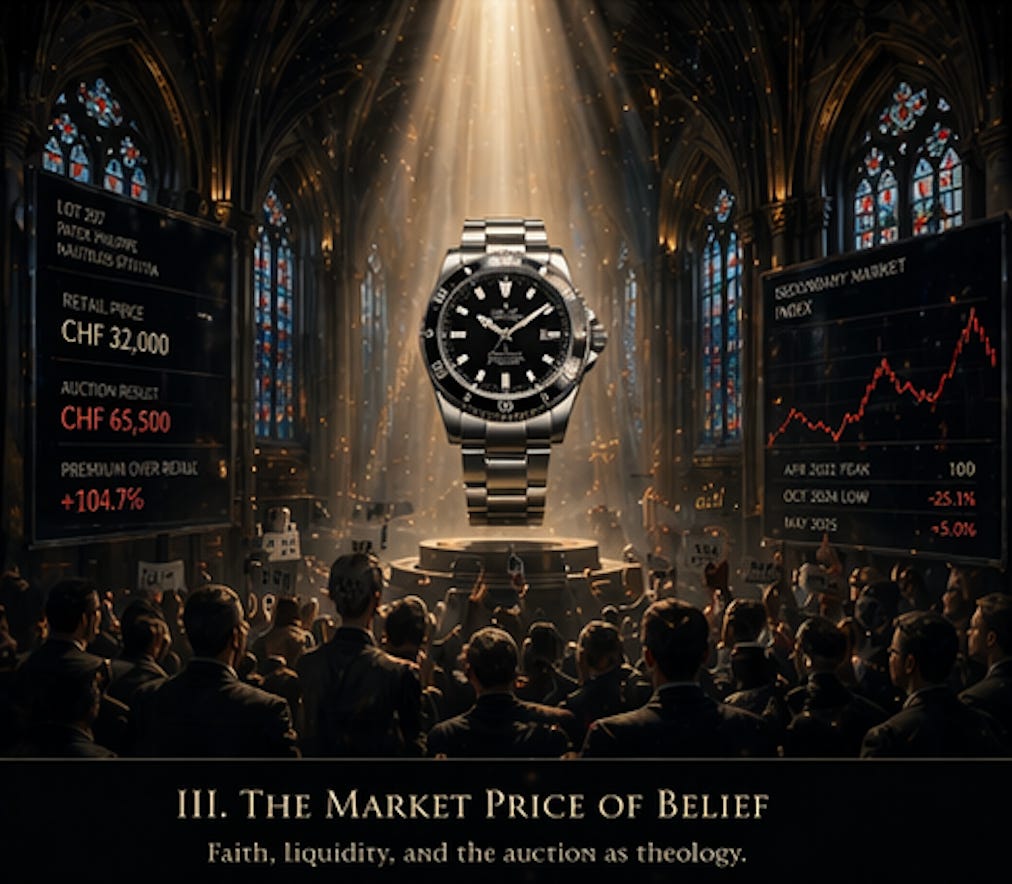

Consider two watches on a dealer’s desk. The first is a Vacheron Constantin Overseas, made by the oldest continuously operating watchmaker in the world. Its movement carries the Geneva Seal, which certifies that every visible component has been finished to the most exacting standard in Swiss horology. The rotor is hand-engraved in twenty-two-carat gold,…