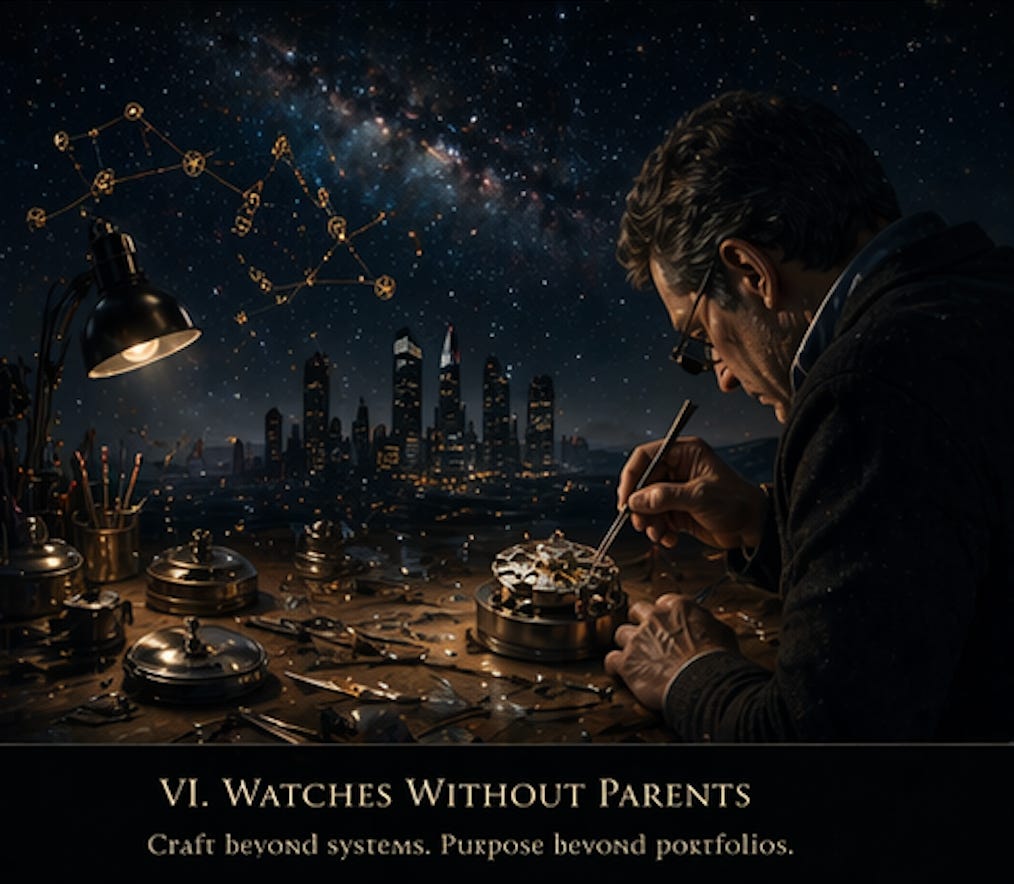

François-Paul Journe produces approximately one thousand watches a year. Rexhep Rexhepi, working from a small atelier in Geneva’s old town, makes perhaps thirty. Roger W. Smith, on the Isle of Man, makes fewer than ten. Philippe Dufour, widely regarded as the greatest living watchmaker, has effectively ceased production. These are not brands in any sens…